Check out this website I found at this link

Friday, October 14, 2011

What Is Technical Analysis? | 360 Stock Charts

What Is Technical Analysis?

Typical Stock Chart

Technical Analysis is the study on how security prices behave and how to use that information to trade and avoid losses. Technical analysis illustrates the classic economic theory of supply and demand in a visual manner, that also has a predicative value in its ability to forecast future price movements, or trends, often based on probabilities and sentiment in the markets. So instead of reading a company’s financial statements or analyzing the industry conditions, technical analysis focuses on the emotions and behaviors of the company’s investors.

It is like visual investing or a visual representation of how a stock behaves over time.

Technical analysis, or stock charting, utilizes a wide variety of indicators to help predict the future movement of a stock, for example, the relative strength index or RSI, moving average convergence-divergence, or MACD, and regressions.

WHAT IS TECHNICAL ANALYSIS?

Technical Analysis is the study on how security prices behave and how to use that information to trade and avoid losses. Technical analysis illustrates the classic economic theory of supply and demand in a visual manner, that also has a predicative value in its ability to forecast future price movements, or trends, often based on probabilities and sentiment in the markets. So instead of reading a company’s financial statements or analyzing the industry conditions, technical analysis focuses on the emotions and behaviors of the company’s investors. It is like visual investing or a visual representation of how a stock behaves over time. Technical analysis, or stock charting, utilizes a wide variety of indicators to help predict the future movement of a stock, for example, the relative strength index or RSI, moving average convergence-divergence, or MACD, and regressions. Just as there are many indicators there are also many techniques, for example, candle stick charting, Dow Theory and Elliott wave theory. No one indicator or method is sufficient to guarantee profits on every trade, so the investor must learn and then decide which indicators and methods to use in his or her analysis, and then apply them with a disciplined approach. Technical analysis is one of two broad categories of analysis, the other being fundamental analysis. Some authors will try and tell you that technical analysis is only used for short-term or speculative purposes. I do not agree! Technical and fundamental analysis are siblings: Once you perform your fundamental analysis and identify potential investment opportunities, you can use technical analysis is identify entry and exit points of your investments. Think of technical analysis in this matter: How do you know whether the price today is good or bad? By comparing it to the past and forecasting into the future. Technical analysis allows you to do both. You can look at the current price in relation to the past, or historical prices, and project the current trend or direction of the stock into the future. And technical analysis goes way beyond these basic principles. It allows you to determine whether a stock is overbought or oversold, long- and short-term trends, trading ranges, and even measure sentiment. Lastly, since most of us think and see with our eyes, technical analysis allows us to ‘see’ an investment in real-time. Good investing, Kevin of the 360 Investing Guys

Sunday, August 14, 2011

What is value investing?

By Nimi Akinkugbe

Value investing is an investment approach that is based on the premise that with some effort, you can find good, strong companies whose share prices have fallen, so offer good value for money. It was made popular by Benjamin Graham, and Warren Buffet, who largely based his investment decisions on the tenets of value investing and used this approach to build his extraordinary fortune. According to Warren Buffet, “value investing is the real form of investment, anything else is pure speculation.”

Assumptions of value investing

More often than not, the stock price does not reflect the real value of the stock itself. Market volatility, emotions and fear drive price volatility. The result is that stock prices will be either overvalued or undervalued at a particular time.

Nobody knows exactly when the market will reflect the stock’s true or fundamental value; it could take months, years, even decades. However, its future prospect and potential growth is the best indication of a stock’s true value. Fundamental analysis helps one in uncovering hidden gems in the stock market. Such companies would usually have valuable assets, a strong balance sheet reflecting stable earnings and dividend history with potential for growth, an experienced board and management team, and would command a sizeable market share. How a company’s financials stand, its credit ratings, and industry outlook; all these come into play and are key to fundamental analysis.

Value investing is somewhat subjective and two investors may have exactly the same information on a company and yet place differing values on it using different valuation methods. Companies of different sizes or in different sectors may differ in terms of what is considered to be of good value. For example, what is cheap for a banking stock may not be cheap for a company that produces consumer goods.

Value investing thrives on fear and uncertainty

Markets often over react to negative news with the result that good stocks fall far below their fundamental values along with less attractive stocks. Value investing relies on the psychology of fear in the market. When there is fear in the market, many “investors” start to sell in a panic. In this process, some attractive stocks fall below their fundamental values ready to be snapped up by the discerning value investor.

Bargain hunters

Value investors are often labelled “bargain hunters” as they actively seek out the stock of companies that they believe are undervalued; they are not just looking to buy cheap stocks but are “smart” shoppers looking for the stocks of companies with good fundamentals. When they are undervalued, they buy them, and where they are overvalued, they stay away from them.

The Cash advantage

As far as possible, it is advisable for investors to hold some cash in their portfolios at all times. Stockmarket investing comes with a degree of risk. It is thus important to hedge your risks by diversifying your investment portfolio to include not just stocks but other asset classes such as bonds, real estate and cash; this helps reduce volatility in your portfolio and protects your net worth. Value investors with cash holdings in their portfolio have the luxury of buying great stocks at relatively low prices during a market correction or crash; this can lead to a solid appreciation in their portfolios over a longer period of time.

Think long term

Markets tend to overreact to good and bad news and price movements may not necessarily correspond with a company’s long-term prospects. Value investors believe that although the stock market may be volatile in the short-term, and may not capture the fundamentals of a business, in the long-run, the fundamentals are of paramount importance. This is not about making quick money; thinking long term forces you to think more about quality. As Warren Buffet comments, “Great investment opportunities come around when excellent companies are surrounded by unusual circumstances that cause the stock to be mis-appraised.” Uncertainty favours long term value investors as it creates fear, leading to panic selling, which forces prices downward regardless of a company’s long term prospects. They are better able to weather the storm of market volatility as they expect that its long term economic value should eventually pull a company’s stock price back up; it doesn’t matter that its share price goes down temporarily.

Are you still apprehensive about the stock market?

Many people continue to be apprehensive about the stock market, yet we are experiencing a time that can be described as the value investors’ dream as we continue to see real discounts among companies with strong underlying fundamentals offering significant buying opportunities. Many companies have hit unprecedented lows in their share prices and some of them represent good value that make them attractive buys for the serious long term investor, in spite of the fact that their share prices could still drop further.

It is important to adopt an investment strategy that will guide your overall investment decisions about which stocks to purchase and when to buy or sell. The style that you ultimately choose should largely depend on your objectives, your expectations of long-term returns and your risk appetite.

Equipped with the right tools, knowledge, research and of course, professional support, you can equip yourself to make better informed decisions. For most investors however, it is far simpler to take advantage of the opportunities that exist by accessing the market through mutual funds and discretionary portfolios where all decisions are made on your behalf by experienced professionals.

via 234next.com

A very timely article by Nimi Akinkugbe given the recent market turmoil we have been experiencing. We've got hundreds of emails the last few weeks asking whether we are up or down in this market. Regardless of your investing approach, you should always have some cash on the side lines to create options for yourself if the markets pull back. Yes, value investors might be getting hit hard with this recent market pullback, but it also creates a great opportunity for value investors to find great discounts for some of the best companies.

Happy Investing,

The 360 Investing Guys

Sunday, August 7, 2011

A Five-Step Checklist for Turbulent Markets

One of my favorite investment sayings is attributed to value investing legend Shelby Cullom Davis: "You make money during bear markets; you just don't know it at the time."

Davis' point, much like Warren Buffett's oft-quoted "be greedy when others are fearful" advice, is that opportunistic contrarians can set their portfolios up for great returns by buying when and what others are selling.

Unfortunately, many investors also lose their money during weak markets. They panic-sell and upend what had seemed like sensible investment plans when cooler heads prevailed. Then, when the market inevitably begins to ascend again, they're left with that nagging question: Is now the time to get back in? I'm still getting emails from people who moved to cash during the last downturn.

But telling people to stay cool or go run around the block (my mom's favorite advice for restless kids) can seem platitudinous on days when the market drops by 500 points. And let's face it--as with most weak markets, there are scary headlines out there: gloomy economic news here at home, combined with concerns that Europe's current debt crisis is more widespread than initially feared. If you were among those many investors compulsively hitting "refresh" on your computer for market news on Thursday and Friday, I can hardly blame you.

One way--really the only way--to stay grounded at times like this is to concentrate your energies on your own portfolio and your own financial status. Changes may indeed be in order for your investment program, but you won't know that without conducting some analysis. Your best first investment during turbulent markets is an investment of time. You want to invest in time to see where you stand now, and, if you determine changes are in order, thoroughly research your options.

Here's your five-step checklist for times such as these.

Step 1: Check adequacy of cash reserves.

By far the best way to manage your portfolio--and your emotions--during volatile markets is to make sure that you have adequate cash on hand to cover your near-term needs. That way, your long-term stock investments can do what they're going to do, but you can take comfort in knowing that it won't affect your ability to pay your grocery tab or the bill for next year's college tuition. For retirees, that means that you need to hold one to two years' worth of living expenses (those expenses that are not covered by any other regular income you have coming in the door) in cash.

You can then stage the rest of your money in progressively more aggressive/long-term investments. (This article discusses how to employ what's often called a "bucket" approach to retirement income.) Folks who aren't yet retired can run with smaller amounts of cash--three to six months' worth of living expenses, plus enough to cover any near-term bills that you can't fulfill with your regular paycheck is a good rule of thumb. Don't include any residual cash in your long-term investment holdings--such as stock or bond funds that are holding cash--when you do your tally.

Step 2: Check your long-term positioning.

Once you've done the liquidity check, the next step is to check the asset allocation of your long-term assets. Market sell-offs can be alarming for retirees and people getting close to retirement simply because they typically have more money invested, period, than do their younger counterparts. For example, someone with an $800,000 portfolio that's split 60/40 between stocks and bonds would've lost about $25,000 on Thursday alone. But particularly jarring losses can be symptomatic of a problem that needs addressing. You might have too much in stocks given where you are in your life stage; this article provides some guidance for making sure your stock/bond split is in the right ballpark.

Alternatively, you might have your asset allocation right, but your subportfolio allocations skew too heavily toward aggressive investments. For example, your equity portfolio might lean heavily on small- and mid-cap stocks or your bond portfolio has too big an emphasis on corporate bonds rather than the government issues that tend to hold up better when recession worries grip the market. Morningstar's Instant X-Ray tool can help you identify unintended bets that expose your portfolio to extra risk.

Step 3: Initiate defensive hedges with care.

As the stock market has swooned, a very small handful of the usual suspects have actually benefited: gold, U.S. Treasury bonds, and bear funds that are shorting stocks. I hope the long-term performance pattern from bear funds is enough to deter you from monkeying with one of these investments; nearly every fund in the group has a negative to scarily negative five-year return, and these funds' short-term performance gyrations can also be unnerving. Gold and Treasuries, meanwhile, can serve a much more legitimate defensive role in a portfolio. The problem with them, however, is that both investment types have already enjoyed a sizable runup. So if you're moving into either, do so very slowly, and only after you've checked your existing exposure to those asset classes; if you own funds run by active managers, those managers might have already beaten you to the punch.

Step 4: Make sure you're taking advantage of "gimmes."

In unsettling times, the most empowering strategies are those that stick within your sphere of control. Checking your long-term asset allocation and cash reserves clearly falls under the "in your control" heading, and so does carefully calibrating what you put into--and what you take out of--your portfolio. It might seem obvious, but boosting your own savings rate (or making sensible cutbacks to your withdrawal rate, if you're already retired) is a guaranteed way to increase the size of your nest egg. So if you haven't revisited your contribution rate for a while, now is a good time to do so. It also makes sense to prioritize saving within any tax-sheltered wrappers you have available to you; Roth IRAs and 401(k)s are particularly sensible if you're concerned that taxes could head higher in the future.

Step 5: Develop a strategy for deploying cash.

Now, back to the Shelby Cullom Davis quote that I used to kick off the article: The best way to make money is to be willing to invest when others are afraid to do so. So if you have cash to invest or are in the process of moving around already-existing holdings, do so with a contrarian mind-set. We've recently published a series of articles and videos about ![]() stocks and ETFs that appear attractive to our analysts on a bottom-up basis. I'm also a big fan of Morningstar's Market Fair Value graph and

stocks and ETFs that appear attractive to our analysts on a bottom-up basis. I'm also a big fan of Morningstar's Market Fair Value graph and ![]() ETF Valuation Quickrank when I need to get a quick read on what parts of the market appear cheap and which parts are still pricey.

ETF Valuation Quickrank when I need to get a quick read on what parts of the market appear cheap and which parts are still pricey.

Original article via here

With the current turbulence in world and local financial markets, now more than ever a disciplined approach to investing is vital. An excellent article, mind you a bit advanced for beginner investors, from Christine Benz, director of personal finance, on Morningstar. We're here to break this down for you, feel free to keep leaving us questions by email or here on the blog.

Happy Investing,

The 360 Investing Guys

Thursday, July 28, 2011

Beach books for investors interested in the classics

Beach books for investors interested in the classics

As we are savouring the nice days of summer, perhaps it's a good time to review great books written on investing in the stock market. You are maybe wondering what to bring to the beach to read. Why not read about the principles of sound investing? It will perhaps help you to someday own a beach!

There are many great books out there. In the last few years, there have been legions of new books written about investing (not all equally good). But I'll start with the classics.

The first book to read is The Intelligent Investor. It was written in 1949 by Benjamin Graham, known as the "father of fundamental analysis." That book deeply influenced Warren Buffett (he likes to say that it changed his life). It is a book about investment principles, and you know what they say about principles: If they change they are not principles in the first place. More than 60 years have passed since Graham wrote this book and his principles are as valid today as they were then. For example, there is a complete chapter on the investor and how he should deal with market fluctuations (the famous Chapter 8). And in the conclusion, there is perhaps the most important phrase written about stock market investing: "Investing is more intelligent when it is most business-like." It means that owning stocks is about owning fractional parts of a business. And the more intelligent an investor is, the more like a business owner he behaves.

There is also an older book written by Philip Carrett in 1930: The Art of Speculation. Although the word speculation is used, Philip Carrett was a long- term investor. His list of 12 commandments is still relevant today. My personal favourite is: "Be quick to take losses and reluctant to take profits." As we get more experienced with markets, we realize how important this phrase becomes.

A totally different approach was developed by Philip Fisher, who lived on the West Coast. He wrote four books. The first one - and most famous - is Common Stocks and Uncommon Profits. It is probably the first book written on investing in "growth" stocks. In the 1960s, he published Path to Wealth Through Common Stocks and in the 1970s, Conservative Investors Sleep Well. They are all very good. Fisher had a deep focus on the quality of management. Again, it's all about principles. Many companies that Fisher refers to do not exist anymore (at least in their original form) but the numerous examples are quite instructive.

In the 1980s, John Train wrote two great books on Money Masters. The first one talks about Warren Buffett (at a time when he was unknown by most investors), John Templeton and Ben Graham.

There are dozens of books written about Buffett and a lot of redundancy is out there, but there are three that I would recommend: Warren Buffett: the Making of an American Capitalist by Roger Lowenstein, The Warren Buffett CEO by Robert P. Miles and Of Permanent Value by Andy Kilpatrick. This last one is quite a detailed book on everything regarding Buffett (it has more than 1,000 pages). In the spirit of full disclosure, I must confess there is a little chapter on my career and the influence of Buffett on my life in this book.

Recently, I have enjoyed books written by James Montier. My favourite is Value Investing: Tools and Techniques for Intelligent Investment. It was published in 2009, so it is quite timely in many of its studies.

Another recent book that I enjoyed is This Time is Different: Eight Centuries of Financial Folly by Carmen Reinhart and Kenneth Rogoff. This book provides a lot of historical perspective on the 2008-2009 crisis. We realize how much financial crises are part of our capitalist system and - although not pleasant - how they should be accepted and dealt with.

Finally, I would recommend reading Peter Lynch's books. They are instructive and also written in a more convivial style than the others. The most famous one - and still the best - is One Up on Wall Street. When I read that book, almost 19 years ago, it changed my life. It gave birth to a passion for stock investing that has not left me since.

Francois Rochon is the head of wealth-management firm Giverny Capital, which he founded in 1998.

Montreal Gazette

© Copyright (c) Postmedia News

Original article content via vancouversun.com

A great summary in the Vancouver Sun today! I've read all these books and highly recommend both the Intelligent Investor and of course Common stocks and Uncommon Profits! Great books for beginner investors who want to get into the investing game... all these books are available on amazon.com

Happy Investing,

The 360 Investing Guys

Thursday, July 21, 2011

Bolster Your Portfolio With Dividend Stocks

By Evan Sundermann

#1 – Understand the Importance of Dividends

In today’s market, relying on capital appreciation in order to achieve investment goals is increasingly difficult. It is exceedingly important for all types of investors to bolster their portfolios by adding stocks that pay dividends in order to position their investments to deliver reliable gains. If executed properly, investing for income can help investors build positions over time and add to their capital through Dividend Reinvestment Plans (DRIPs) or provide them with a steady inflow of cash throughout the year. In addition, dividends can provide investors with steady, stable gains during times of global and economic uncertainty that has the ability to wreak havoc on the market.

#2 – Invest, Don’t Speculate

“The Intelligent Investor”, written by professional investor and economist Benjamin Graham, has influenced some of the world’s most successful and famous investors, including Warren Buffett, who calls it “by far the best book on investing ever written”. In the book, Graham advocates a conservative approach to investing centered upon the idea that

An investment operation is one which, upon thorough analysis promises safety of principle and an adequate return. Operations not meeting these requirements are speculative.

When researching companies and securities prior to making an investment decision, it is imperative to avoid searching for stocks that you are counting on to significantly outperform the market. This type of aggressive speculation involves assuming unnecessarily high levels of risk and often results in a substantial loss of capital.

#3 – Be Conservative

Investing doesn’t have to be feast or famine. If you take the emotion out of investing and refuse to buy into any get rich quick schemes or ideologies, then you have a great chance to build wealth through educated and conservative investing.

While small-cap and mid-cap stocks are often targeted by aggressive investors seeking a high return from capital appreciation, large-cap and blue chip stocks are typically safer investments and are preferred by investors eyeing dividend income. One of the most important aspects when investing for income is identifying companies that have large enough cash reserves and revenue streams to allow them to consistently pay out dividends and reward their investors by increasing their yields. While researching securities focus on large-cap stocks and blue chips.

Criteria & Considerations to Explore Prior to Investing:

Financials & Dividend History:

Avoid only looking at companies currently paying high yields. Try to find companies with respectable yields in addition to a history of increasing dividend yields and not missing payments. Stocks that meet this criteria typically prove to be safer, more reliable investments.

You may want to examine financial statements and look at figures such as the companies cash reserves and debt on the balance sheet, or sales, expenses, and net income on the income statement. One specific financial ratio that may be of use to investors as they research stocks is the payout ratio, which is calculated by taking Dividends per Share and dividing them by Earnings per Share. High dividend yields in the present to do not always guarantee high or increased dividend yields in the future. The payout ratio allows investors to contemplate the likelihood of a company increasing its yield to investors in the years to come.

Products & Services

Invest in companies that produce products or provide services that appeal to, or are needed by, a wide variety of consumers.

Stay away from companies that provide trendy products or services that have not proven their ability to retain strong demand. Consider whether or not you believe that a company’s products and services will maintain their appeal and demand amongst their target demographic over the course of the next several decades. Tastes and preferences among consumers fluctuate frequently, and competitors are likely to enter the market and attempt to gain market share if demand and profits persist.

Business Model & Staying Power

Steer clear of companies whose products or services may become irrelevant down the road due to technological advances. Consumer staples and energy are two industries that provide some of the best investment opportunities; however, there are worthy investments to be had outside of these two industries as well.

Remember that you are not just buying stock, you’re investing in a company's potential to generate future earnings. Identify companies that you want to own for decades to come.

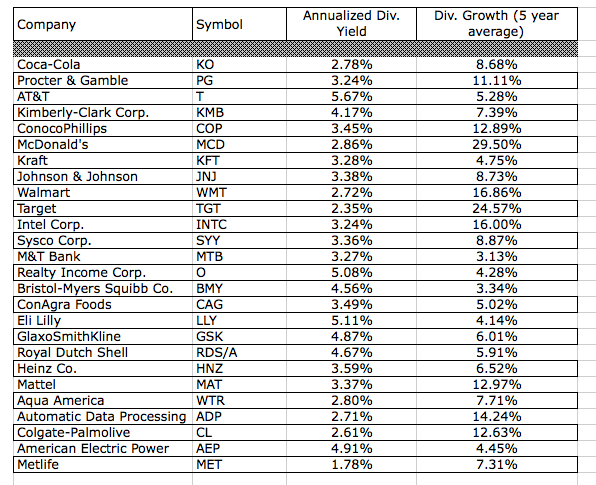

Below I will examine a variety of blue chip stocks that have proven to be dividend champions, boasting high yields that have increased on a regular basis, proven business models, strong financials, and unwavering demand. Also, look at the chart provided that lists several other stocks of interest that meet the criteria of the conservative income investment strategy outlined above.

Coca-Cola (KO)

Coca-Cola is the giant of the beverage industry with a market cap of $154.59 billion. Coke stock currently has an annualized dividend yield of 2.78%. Although this yield is not stunning, Coca-Cola has increased its yield by an average of 8.68% each year over the past five years and you don’t have to worry about them missing a payment any given quarter.

As far as brand names go, Coca-Cola is one of the most recognizable brands in the world. Coke’s business is going strong; on July 19th they announced that second quarter profits for 2011 rose 18% due to recent acquisitions and strong international sales. If you’re looking for a blue chip stock with a solid yield that you can expect to grow steadily in the years to come, Coca-Cola is a great choice.

Coca-Cola pays dividends to its investors quarterly in March, June, September, and November.

Procter & Gamble (PG)

Procter & Gamble’s 50 brands produce just about every household item you can imagine, including laundry detergent, dog food, paper towels, shampoo, razors, bleach, batteries, diapers, toothpaste, air freshener, over the counter medications, etc. P&G stock currently yields an annualized 3.24% and has shown a commitment to growing its yield, averaging an increase of 11.11% annually of the past five years. P&G produces the kind of consumer staples that most income investors look for and offers a very respectable yield for such a safe investment.

Procter & Gamble pays dividends to its investors quarterly in January, April, July, and October.

AT&T (T)

AT&T is far and away the largest company in the telecom industry with a market cap of over $179 billion. Cellular devices are revolutionizing the way people interact and demand for AT&T’s products and services will continue to grow as standards of living and infrastructure improve in emerging markets. AT&T currently yields a robust 5.67% to investors annually and has continued to grow its yield by an average of 5.28% each of the previous five years.

AT&T pays dividends to its investors quarterly in January, April, July, and October.

Kimberly-Clark (KMB)

Kimberly-Clark produces household and personal care items, including recognizable brands such Kleenex, Huggies, and Scott. The Dallas based company boasts a 4.17% annualized yield and has increased its yield by an impressive average of 7.39% over each of the past five years. Kimberly-Clark, like Procter & Gamble, produces consumer staples that provide for a safe and stable investment to go along with reliable dividend income.

Kimberly-Clark pays dividends to its investors quarterly in January, April, July, and October.

ConocoPhillips (COP)

Although smaller than rivals such as Exxon Mobil (XOM), Chevron (CVX), BP, and Shell (RDS.A), ConocoPhillips is still in the upper echelon of oil and gas companies with a market cap of over $108 billion. Naturally, oil companies make more money when oil prices are high and less when prices dips but ConocoPhillips is a diverse and large enough company to withstand the constant fluctuations that occur within the energy sector.

Currently, ConocoPhillips stock yields 3.45% annually and has boosted yields by an impressive average of 12.89% annually over the past five years. The company is currently expanding its drilling in shale fields in the United States and if their bet pans out then you can expect ConocoPhillips to increase their yields even further.

ConocoPhillips pays dividends to its investors quarterly in March, June, September, and December.

McDonald’s (MCD)

McDonald’s is considered one of the “Dogs of the Dow”, meaning it is one of the ten highest yielding stocks in the DJIA. The fast-food company currently offers investors an annualized yield of 2.86% but has increased its yield by a hefty average of 29.50% annually of the last five years. McDonald’s is well established in the United States and is booming overseas with continued growth in developed countries and expansion into emerging markets. Expect McDonald’s growth to serve as a catalyst for the company to continue increasing its yield to investors.

McDonald’s pays dividends to investors quarterly in March, June, September, and December.

click to enlarge

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

via seekingalpha.com

Good article by Evan Sundermann. A nice recap of some good value investing stocks to consider if you are a first time investor. Over the long run, you will find many of these stocks have steadily increased in value, often times splitting, and in most cases paying back their investors with strong dividends. An added bonus, most have steadily increased their dividend pay-outs year after year.

Happy Investing,

The 360 Investing Guys

Disclosure: The 360 Investing Guys have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours either.

Saturday, July 16, 2011

Buy what you understand

Buy what you understand

As disciples of Warren Buffett and Charlie Munger, GFI Investment Counsel CEO Daniel Goodman and vice president Effie Wolle focus on value. They look for businesses with a sustainable competitive advantage at a reasonable price. And when the company is good enough, they are willing to pay a bit of a premium.

“If you are buying a greatquality business with a durable competitive advantage, I think it is okay to pay up,” Goodman says.

Finding good management is another focus at GFI, as is avoiding serious capital depletion.

“It’s not always about what you buy, it’s about what you don’t buy.” Goodman says, adding that GFI watches the Street but does all its own analysis.

“We try to invert the situation, especially when it is an issue brought out by corporate finance or an investment bank,” he adds. “Why are they raising money? Why are they diluting equity stakeholders?”

Wolle stresses that GFI sticks within its circle of competence, avoiding names like Sino-Forest Corp., Yellow Media Inc. and Research In Motion Ltd.

“We avoid dying industries or business models that are too difficult to understand,” he says.

In the first six months of 2011, private client accounts rose roughly 4% to 6% by owning quality companies that pay good dividends -and avoiding the bad ones.

The managers will do some opportunistic trading as well as take short positions in the Good Opportunities Fund. It has the same approach as private client portfolios.

The fund currently has a higher-than-average cash position of around 24% due to the sale of a favourite name, international shopping warehouse club company PriceSmart Inc., which has risen very dramatically.

“I don’t think the cash level is a macro call -expecting the market to bottom out,” Goodman says. “It’s just a question of our comfort level.”

“We’re not finding any great things to do with the money, so we hold the cash,” Wolle adds.

Holding a significant cash position is a typical defensive strategy. These days with low interest rates some say it doesn't get you very far. But how does a 1% gain or a 0.50% gain look against a 5-10% loss? That's the decision that investors have to make when markets are pulling back or are volatile for macroeconomic reasons...

Happy Investing,

The 360 Investing Guys

Wednesday, July 13, 2011

4 Tips in Assessing Company’s Management

SEDI in Canada allows you to look up management's stake in various companies. The SEC also has similar disclosures/registrations that are publicly available to check management's stake in the game. Some online discount brokers also have alerts or allow for you to check management insider trading, which is always a very good indicator of what might be going on behind the scenes!

In general, investors don't like or appreciate surprises. A strong management is usually one who is consistent in their plans and delivery of results. Watching a company's press releases is the best way to understand this and apply it practically.

Happy Investing,

The 360 Investing Guys

Sunday, July 10, 2011

Investing 101: How to Grade a Company's Management Team

Investing 101: How to Grade a Company's Management Team

A company’s management team is meant to run their company in the best interests of the owners. This means using the company’s assets and the stockholders’ investment efficiently and, in turn, producing a fair return.

Often, the interests of management and the interests of owners do not meet eye-to-eye. In a theoretical sense, management wants to maximize their personal wealth while the company’s owners want to maximize the company’s profitability. Sometimes this can lead to a mismatch in how management runs a company and how management should run a company.

For instance, management can become too conservative. If management is too concerned with the risk of projects in their pipeline, they may say “no” too many times and not use their assets effectively. Management could also become too risky if they feel they have nothing to lose and risk losing part of their revenue stream.

Luckily there are a few simple ratios to measure how well management is doing. Two of the most commonly used ones are:

(ROA) Return on Assets = Net Income / Assets

(ROE) Return on Equity = Net Income / Equity

ROA measures the return from using the company’s assets for one year, while ROE measures the one-year return from stockholder’s historical investment in the company. Companies that have higher ROA and ROE than their industry peers most likely have management teams that are above par. And if a company is seeing increases in ROA and ROE over time, it also bodes well.

To illustrate the use of these ratios, we ran a stock screen on companies that have seen increases in both ROA and ROE year-over-year. We then screened for those that have also seen significant net buying from institutional investors (a.k.a. the “smart money”).

Do you think these companies are being run well? Use this list as a starting-off point for your own analysis.

Analyze These Ideas (Tools Will Open In A New Window)

1. Access a thorough description of all companies mentioned

2. Compare analyst ratings for all stocks mentioned below

3. Visualize annual returns for all stocks mentioned1. Microsoft Corporation (MSFT): Application Software Industry. Market cap of $216.05B. During the current quarter, institutional investors have been net buyers of 314.3M shares, which represents 4.21% of the company's 7.46B share float. TTM ROA at 23.61% vs. prior-TTM ROA at 22.49%. TTM ROE at 43.96% vs. prior-TTM ROE at 41.83%.

2. Oracle Corp. (ORCL): Application Software Industry. Market cap of $164.11B. During the current quarter, institutional investors have been net buyers of 141.4M shares, which represents 3.63% of the company's 3.90B share float. TTM ROA at 12.65% vs. prior-TTM ROA at 11.26%. TTM ROE at 24.22% vs. prior-TTM ROE at 21.95%.

3. Imperial Oil Ltd. (IMO): Oil & Gas Refining & Marketing Industry. Market cap of $38.70B. During the current quarter, institutional investors have been net buyers of 8.0M shares, which represents 3.11% of the company's 257.42M share float. TTM ROA at 12.47% vs. prior-TTM ROA at 10.14%. TTM ROE at 23.17% vs. prior-TTM ROE at 18.78%.

4. Starbucks Corporation (SBUX): Specialty Eateries Industry. Market cap of $29.56B. During the current quarter, institutional investors have been net buyers of 14.7M shares, which represents 2.01% of the company's 729.89M share float. TTM ROA at 16.65% vs. prior-TTM ROA at 13.36%. TTM ROE at 27.86%vs. prior-TTM ROE at 24.64%.

5. Cognizant Technology Solutions Corp. (CTSH): Business Software & Services Industry. Market cap of $22.23B. During the current quarter, institutional investors have been net buyers of 2.3M shares, which represents 0.76% of the company's 303.01M share float. TTM ROA at 19.40% vs. prior-TTM ROA at 19.31%. TTM ROE at 23.77% vs. prior-TTM ROE at 23.12%.

6. Intuitive Surgical, Inc. (ISRG): Medical Appliances & Equipment Industry. Market cap of $14.47B. During the current quarter, institutional investors have been net buyers of 427.1K shares, which represents 1.10% of the company's 38.78M share float. TTM ROA at 17.47% vs. prior-TTM ROA at 17.03%. TTM ROE at 20.03% vs. prior-TTM ROE at 19.68%.

7. Check Point Software Technologies Ltd. (CHKP): Security Software & Services Industry. Market cap of $13.69B. During the current quarter, institutional investors have been net buyers of 379.4K shares, which represents 0.24% of the company's 160.62M share float. TTM ROA at 13.97% vs. prior-TTM ROA at 12.90%. TTM ROE at 18.29% vs. prior-TTM ROE at 16.67%.

8. Analog Devices Inc. (ADI): Semiconductor Circuits Industry. Market cap of $11.48B. During the current quarter, institutional investors have been net buyers of 395.7K shares, which represents 0.13% of the company's 293.75M share float. TTM ROA at 19.41% vs. prior-TTM ROA at 13.46%. TTM ROE at 27.25% vs. prior-TTM ROE at 17.24%.

9. Expeditors International of Washington Inc. (EXPD): Air Delivery & Freight Services Industry. Market cap of $10.69B. During the current quarter, institutional investors have been net buyers of 4.2M shares, which represents 2.01% of the company's 209.04M share float. TTM ROA at 14.23% vs. prior-TTM ROA at 10.83%. TTM ROE at 21.61% vs. prior-TTM ROE at 15.97%.

10. Chipotle Mexican Grill, Inc. (CMG): Restaurants Industry. Market cap of $9.47B. During the current quarter, institutional investors have been net buyers of 647.1K shares, which represents 2.12% of the company's 30.59M share float. TTM ROA at 17.44% vs. prior-TTM ROA at 15.08%. TTM ROE at 23.48% vs. prior-TTM ROE at 20.38%.

(Article written by Alexander Crawford. List compiled by Daniel Guttridge)

Please follow Money Game on Twitter and Facebook.

Follow Kapitall on Twitter.

The quality of a company's management is vital in assessing its future performance, from a value investing perspective. Can management be trusted? This is key because it gives you two important pieces of information:

1) Can I rely on the historical information management is presenting? and

2) Can I rely on the future predictions management is making?

Both of which drive a company's news and stock price. Poor management leaves room for manipulation of a company's stock price, you often see this in penny stocks, and rarely with larger companies. Although, if you think back to to the Enron and Worldcom scandals in the early 2000s, nothing is off the table.

So how does one assess a company's management? How do you know they are good quality? We plan to cover assessing management in the "Value Investing" module in our upcoming course. Look forward to more of your questions!

Happy Investing.

Friday, July 8, 2011

Columbia Ideas at Work : Feature : Value+Investing's+Long+Run

The finance discipline is in the process of a halting transition. The efficient markets/modern portfolio theory is giving way to broader perspectives that incorporate the realities of information asymmetry — the fact that all market participants do not have the same access to relevant information — and deeply ingrained behavioral biases that often dominate actual financial market outcomes. At the leading business schools these latter approaches are now firmly established even though in the finance profession at large they remain relatively unfamiliar.

One particular aspect of this change is the increasing importance of value investing, an approach to investment management pioneered by Benjamin Graham and David Dodd ’21 at Columbia. In part, this is due to the overwhelming success of the value approach in practice. Individual value investors like Warren Buffett and value-oriented institutions like Sanford Bernstein populate the ranks of outstanding investors out of all proportion to their numbers. However, it is also due to a detailed appreciation of the way value investing differs from more conventional approaches, how this is responsible for the historical success of value investors, and why it is likely to continue in the future.

Traditional characterizations of value investing have been overly simplistic. Value investing involves buying securities at one-third or greater discounts to their “true” values, effectively buying dollar bills for fifty cents. More recently we have begun to appreciate how a value approach is distinct in the particular areas of searching for investment opportunities and valuing companies.

In search, the value strategy is to look in areas that are obscure, boring, unattractive, and therefore cheap by common metrics like low market-to-book and PE ratios. Simple statistically constructed portfolios of such stocks produce above average returns in cross-sections of securities over all extended time periods in all global markets. (My colleague Tano Santos shows this in his take on the question.) In time-series, there are reliably predictive levels of positive serial correlation in short-term returns. Neither phenomenon should be observed if markets were perfectly efficient. (Attempts have been made to associate the higher cross-sectional returns of “cheap” stocks with higher levels of risk, but these risk factors never turn out to be empirically measurable independent of cheapness.) Behavioral research phenomena such as loss-aversion, overconfidence, and lottery preference — the disproportionate desirability of low probability, very high reward outcomes — account for the value of “cheapness” much more directly. These behavioral approaches suggest that value strategies that focus on undesirable, boring, ugly, and hence, “cheap” areas like distressed securities deserve special attentions, and are likely to continue to be successful as long as the underlying behaviors persist.

In valuation, the discounted cash flow (DCF) approach that business school teach their students has three obvious shortcomings. First, it generally fails to make use of balance sheet information and an approach that ignores potentially significant information will be inferior to an approach that does not. Second, a DCF calculation is a weighted sum of future cash flow estimates. It involves adding good information — the value estimates of near-term cash flows — to bad information — the value estimates of far-future cash flows (typically embodied in a terminal value). The result, as any engineer knows, is that the bad information dominates. A DCF calculation never segregates estimated elements of value by degree of reliability so that reliable elements of value can be separated from unreliable ones. Third, the input assumptions to DCF valuations are parametric — profit margins, revenue levels, growth rates, capital intensities, and costs of capital. There is no easy way to integrate strategic judgments — whether an industry will be viable in the future or whether any firms are likely to enjoy sustainable competitive advantages — into a DCF calculation.

The value approach to valuation — starting with the most reliable information, the balance sheet, to obtain an asset value, then looking at the value of a firm’s present day earnings power, and only then looking at the value of future growth — suffers from none of these deficiencies. It uses all the information (including the balance sheet), organizes that information from most to least reliable (balance sheet to current earnings to future growth in earnings), and is based on a clear relationship between strategic industry judgments and valuation. For example, if a firm does not enjoy competitive advantages in its markets, then it will never sustainably earn above its cost of capital on investments in growth. Under these circumstances growth creates no value and the growth element of value can be ignored no matter how high the growth rate is.

Notwithstanding the statistical evidence, there is an inescapable sense in which markets are efficient. The average return of all investors (before fees) must equal the average return on all assets. Any gains relative to the average by one investor must be offset by the losses of another. Better approaches to search and valuation have placed — and will continue to place — most value investors firmly in the above market part of the return distribution.

Bruce Greenwald is the Robert Heilbrunn Professor of Finance and Asset Management in the Finance and Economics Division and director of the Heilbrunn Center for Graham and Dodd Investing at Columbia Business School.

We will be covering the value approach to valuing a business in upcoming webinars. We'll start with the most reliable information (the audited financial statements) and look at the value of the company's present day earnings power and gauge future growth. A company's balance sheet and income statement can tell you a great about the general health of the business and its future prospects.

Happy Investing!

Thursday, July 7, 2011

Value Investing vs. Momentum Investing: Where Do You Stand?

Value Investing vs. Momentum Investing: Where Do You Stand?

As a professional money manager and stock market radio talk-show host over the last 18 years, it has always been interesting to observe the value vs. momentum debate that takes place in the market. Most of us, whether we are professional investors or individual investors, usually align ourselves with one camp or the other.

Value investors can often times be seen wearing bow-ties or inexpensive suits, and talking at length about stocks trading below their intrinsic value. Value investors probably drive cars that get good mileage and are not afraid to use coupons at the local diner.

Most so-called value investors would recognize the late Benjamin Graham as the "father of value investing." Benjamin Graham was a U.S. economist, professional investor, and professor at the Columbia Business School. Graham also co-wrote the book Security Analysis, which is considered by many to be the bible for serious value investors.

Graham, also wrote the book The Intelligent Investor, which Warren Buffett called the best book about investing ever written. Buffett also called Graham the second most influential person in his life, right behind his father. It should also be noted that Warren Buffett named his son Howard Graham Buffett.

Value investors generally search out stocks with low valuation ratios. Another well-known, present day value investor is David Dreman. In his book, Contrarian Investment Strategies, Dreman did extensive studies that showed over the long haul, stocks with valuation ratios in the bottom quintile far outperformed stocks in the upper valuation ranges.

In other words, his studies showed that the stocks with lowest PE ratios, lowest price to book value ratios, and lowest price to cash flow ratios far outperformed those with highest ratios by a wide margin.

In his book What Works on Wall Street, another well known value investor, James O"Shaugnessy showed that stocks with the lowest price to sales ratios were the best investments over the long haul.

Without a doubt, there is much to be said about true "value disciples" who have racked up some very impressive results over the years. Warren Buffett did not become the richest man in the world by "paying up" for stocks.

Having said this, I have found many flaws in value investing. Many value investors got "their clocks cleaned" during the 2008 financial crisis. A lot of the so-called value stocks at that time were stocks from the financial sector, which absolutely got clobbered that year.

Value investors basically cast a blind eye on performance or momentum. More on value investing later in this article.

Momentum investors, on the other hand, tend to be a little bit more flamboyant. Fast cars, sushi bars and Tommy Bahama are more their style. Instead of Barron's, and Forbes, they read Investors Business Daily. Instead of buying low and selling high, momentum investors buy high and hopefully sell much higher.

Richard Driehaus is widely considered as the "father of momentum investing." William J. O'Neil has also done much to advance the cause of momentum investing with his newspaper, Investor's Business Daily and with his books on investing.

Momentum investing is all about performance, strong technical patterns, and relative strength. O'Neil coined the term "CANSLIM" to sum up the characteristics that he likes to see in a stock:

"C" stands for outstanding current or quarterly earnings comparisons, many times 100% or better.

"A" stands for outstanding annual earning growth, usually in the range of 25% or better. CSCO just does not cut it any more.

"N" stand for something new like a new product, new management, or new high. Sorry Research In Motion (RIMM).

"S" stand for a limited amount of shares outstanding and for those shares available to be in heavy demand. GE would have a hard time making the cut here.

"L" stands for the stock being a leader in their sector or in the market.

"I" stands for heavy institutional ownership. The theory is that it takes heavy institutional demand to drive stock prices higher.

"M" stands for market. Without the cooperation of the market all of the above basically go out the window.

Momentum investing basically closes a blind eye to value. For this reason, momentum investors got killed during the 2000-2002 thrashing that the Nasdaq took. At the Nasdaq peak of April 2000, I remember many, many stocks trading at PE ratios of 100-300 or above. The Nasdaq was at a gaudy 5,300 at that time and now here we are 11 years later and we a little above 2,800.

It has been my observation over the last 18 years in the business that both value and momentum investing have their strong points and their shortcomings. Many times, low PE stocks are nothing more than value traps.

Looking at some of the low forward PE stocks of today, I see a lot of bad stocks:

Microsoft (MSFT) - 9.4 J P Morgan (JPM) - 7.4 Pfizer (PFE) - 9.1 Citigroup (C) - 8.1 Bank of America (BAC) - 6.6 Merck (MRK) - 9.3 Cisco (CSCO) - 9.3 Goldman Sachs (GS) - 7.4 UBS (UBS) - 7.3 Deutsche Bank (DB) - 6.6 AIG (AIG) - 9.3 General Motors - 6.3

Why do I call them bad stocks? These are some of the absolute worst performers in the market. Investors have fared very poorly with them for the last decade.

Here is their respective average annual returns over the last ten years:

Microsoft -(0.4%) J P Morgan +2.2% Pfizer -(3.0%) Citigroup -(19.5%) Bank of America -(6.3%) Merck -(0.5%) Cisco -(1.0%) Goldman Sach +5.9% U B S (-2.0%) Deutsche Bank (-0.7) A I G (-21.6%) General Motors (Starting over!)

Yecch, what a lousy bunch of stocks! If I hear one more so-called analyst on CNBC recommend Cisco, I am going to puke. Oh, I know, the market has basically gone sideways for the last 10 years, but many stocks have excelled during that same period of time. More on this later.

As I stated earlier, I have observed shortcomings in value investing over the years. It is my opinion that many of them deserve to be trading at the low multiples that they currently garner.

It has also been my observation that momentum investing has its flaws. I was there in 2000 when the high-priced momentum darlings got crushed. We found out then that value does matter. Home buyers that were chasing single family homes in 2006 also found out that value does matter, as it may take years for home prices to get back to their 2006 peak.

As I look at some of the highest forward PE stocks at the current time, I can't help but flashback to the year 2000:

Netsuite (N) (136) Lululemon (LULU) (85.6) Clean Energy Fuels (CLNE) (83.2) Salesforce.com (CRM) (79.9) Sinacorp (SINA) (59.4) China Eastern Airlines (CEA) (58.3) Amazon.com (AMZN) (54.8) Open Table (OPEN) (49.1)

These are some very high multiples and they must have fantastic growth to justify such high valuations.

Again, I find big faults with both value and momentum investing.

What is wrong with combining the best attributes of value investing and the best attributes of momentum investing?

What is wrong with buying stocks that still make sense from a value perspective that also are some of the top performers in the market today? Is this possible?

I have developed my own grading system, called the Gunderson Grading System. It assigns a letter grade to 2,700 stocks in the market.

In order for a stock to achieve a Gunderson Grade of "A," it must possess the following attributes:

It must have superior short-term, intermediate-term, and where possible long-term performance on a relative basis against the other 2,700 stock in the market.

It must have a five-year target price that still offers substantial five year upside potential (usually 80% or more).

In determining five-year target prices, I use a very common five-year valuation formula that I used in my days as a securities analyst for many years. The valuation formula begins with next year's consensus EPS estimate (I used to calculate my own on stocks that I followed). Next year's consensus EPS estimate is readily available from many sources. I use Yahoo's website.

I next apply the consensus analyst five-year growth estimate. For an analyst, this growth estimate generally comes from talking with management or by doing your own research on potential market share penetration and the overall size of that market. The five-year consensus growth rate is also readily available from many websites. Here again, I use Yahoo.

I then extrapolate next year's EPS estimate by the five-year growth rate and come up with an EPS estimate for five years down the road. Here is an example of what I mean: Let's assume that stock ABC has a consensus next year EPS estimate of $1.00. Let's also assume that the consensus five-year growth rate from the analyst community is 10%. If everything goes as projected, the earnings over the next five years would look like this:

2012=$1.00 2013=$1.10 2014=$1.21 2015= $1.33 2016=$1.46

In other words, if the company meets next years EPS estimate of $1.00 per share and it does indeed grow at the consensus five-year growth rate of 10% per year, the company would be making $1.46 five years from now.

Now comes the hard part. As a stock analyst, I have to apply a multiple that I think the stock will deserve five years down the road. Another way of saying this would be: "what PE ratio do I think that the stock will be trading at five years from now?"

I wish that there was an easy formula to apply here, but the experience that I have gained by having studied stocks over the last 20 years is invaluable. Nevertheless, here are some tips. A market multiple is generally in the 15 area. This is a good starting point. A superior growth stock can trade at much higher than market multiples however. Consider Netflix (NFLX) or Baidu (BIDU). Netflix currently has a PE ratio of 77, while Baidu has a PE ratio of 79. Also consider, however, that Netflix has been growing its earnings at a 41% clip over the last five years, while Baidu has been growing its earnings by a whopping 93% per year over the last five years.

By comparison, Cisco has been growing its earnings by a very tepid 7% per year over the last five years, while Microsoft checks in at just 13%. No wonder these stocks are trading at such low PE ratios currently. The growth has slowed to a crawl.

Various sectors in the market also trade at different multiples. Technology stocks generally trade at much higher multiples than deep cyclicals. Consumer stocks tend to trade at very close to market multiples, while commodity related stocks tend to trade in the low teens. One can also look at a multiple history or average PE ratio of a stock over the last many years for guidance. This information is also readily available from a variety of sources. Lastly, a look at the current forward PE of a stock, as it can also be a good clue at what multiple a stock deserves.

Once I have the five years from now EPS estimate, I multiply it by the multiple that I think is appropriate for the stock. Let's go back to our $1.46 example. Let's assume that I deem a multiple of 20X to be appropriate for the stock. The stock would therefore have a five year target price of $29.20.

I would only be interested in buying the stock at less than $15 or so. I like to have as close to 100% upside potential over the next five years as possible. The upside potential goes into determining my value grade.

Lastly, I look at how well the stock held up in the year 2008 when the market was under its own stress test. I calculate a safety grade for the stock. I then take into account the short-term performance grade, the intermediate term performance grade, the long term performance grade, the valuation grade, and the safety grade. I also apply a proprietary weighting to each of these grades to come up with an overall Gunderson Grade.

I have been using this grading system for the last several years and could not be happier with the results. I find that "A" rated stocks can remain at the top of the heap for a long time. If their grade starts falling, it may be time to move on. I also find that the grades are a reflection of the current economy. I call my "A" rated stocks the Best Stocks Now. I have also developed a smart phone app and written a book by the same name.

Here are some examples of A rated stocks at the current time:

Green Mountain Coffee (GMCR) - This stock has more than doubled since I bought it. I still have a five-year target price of $175 and the stock has returned an amazing 97.9% average over the last five years and it is still hitting new highs. Without question, it is still a stock of today.

Ezcorp Inc. (EZPW) - There are currently three red-hot pawnshop stocks and EZPW is one of them. In my opinion, this is a reflection on our current economy. I have a five-year target price on EZPW of $68 and the stock has averaged an amazing 47.0% return over the last 10 years.

Tractor Supply (TSCO) - I had the CEO, Jim Wright, on my radio show a several weeks ago, and I can see why this stock has been such an amazing performer. The stock has averaged an amazing 42.4% over the last 10 years and still has roughly 95% upside potential, according to my calculations, over the next five years.

Carbo Ceramics (CRR) - With all of the "fracking" going on across the U.S., it is no surprise that CRR is such a good stock right now. I still calculate almost 90% upside potential over the next five years and the stock has delivered an average return of 22.1% over the last 10 years to its investors.

First Cash Financial (FCFS) - Another pawn shop stock that is running wild right now. Forward PE ratio is just 16.1 and I calculate upside potential of 93% over the next five years. The stocks returned an average of 34% to its investors over the last 10 years.

These are just five examples of stocks that have grades of "A" right now. At any given time roughly 8%-10% or about 200 stocks meet my stringent criteria.

I will write more articles from time to time on stocks that currently have "A" grades in the future.

What are you? A value investor or a momentum investor?

I like them both.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

via seekingalpha.com

Some good illustrations in here, mind you he has chosen specific examples to make his point.

The 360 Investing Guys do not recommend buying/selling any of the mentioned stocks in this article.

Why You Shouldn’t Invest Like Warren Buffett

Why You Shouldn’t Invest Like Warren Buffett

Posted on 06 July 2011.

Note from Managing Editor Sara Nunnally: Everybody knows who Warren Buffett is... The Oracle of Omaha has amassed billions of dollars by buying up stocks at great prices. Sometimes he holds them for years before seeing a big profit.

As a billionaire, he's got the means to do this. He can afford to have a huge chunk of money stay in the market for years at a time. Today's investor, like you and me, has to be more nimble. We have to be able to take profits at a much faster pace.

In this environment, as our guest editor Zachary Scheidt says, "buy and hold" investing is dead. In this environment, we need to be traders...

Zach is the editor of Velocity Trader, and his service just saw a gain of 44% in a single day. Perhaps this is evidence that you should be investing like Zach, and not like Warren Buffett.

Read on! (And don't forget to sign up for Smart Investing Daily and let me and fellow editor Jared Levy simplify the market for you with our easy-to-understand articles.)

Buy and Hold Investing Is Dead

In my previous position as a hedge fund manager, I had one particular client that I will always remember fondly. George was a retired oil driller who had been lucky enough to make some great energy investments, and smart enough to take some profits off the table.

George had a few million dollars invested in one of our funds, and a large position in a single drilling company that he had fallen in love with. What I really liked (most of the time) about George was his predictability.

You see, every Friday afternoon -- without fail -- George would call the office to count his money. A typical conversation would go something like this (keep in mind, George has a thick "Bahstahn" accent):

George: Hi, Zach! How'd we do this week?

Zach: Hi, George... Well, the fund is up about 1.8% for the week and we're looking at a deal that...

George: ONLY ONE POINT EIGHT? C'mon Zach, you ghatta do bettah than that!

Zach: You're right; we'll try to do better next week. We're tracking two different companies that have plans to...

George: What about Atlas (referring to his favorite drilling stock)?

Zach: Well, Atlas is down about 37 cents on the day.

George: What happened??

Zach: Not too much -- the board authorized the second-quarter dividend and...

George: Can you print that out and fax it to me?

Zach: Sure, George. Have a great weekend.

George: (click)

It got to be almost humorous (except for the interruption to my research every Friday). George wanted to know everything about the company -- down to the press releases for each well that was initiated. But he never actually traded the stock. He simply took his lumps when times were bad, and rejoiced when times were good.

The Difference Between Market Environments

During bull market periods, buy and hold works beautifully. Simply pick a successful company (it almost doesn't matter which company) and enjoy the profits as the stock trades higher. The game is easy -- nearly every stock rallies.

If you want better returns, pick more aggressive companies or use leverage (borrowing money to buy more shares). During a bull market, risk doesn't matter. That's because prices continue to tick higher and every pullback is just an opportunity to buy more.

But today's environment is much different. As you should already know, our economy is facing serious risks from a number of different angles:

- Unemployment has been above "acceptable" levels for more than three years now.

- Housing values continue to plummet.

- Food and energy inflation is cutting into consumer as well as corporate spending.

- Emerging market growth is in danger of stalling.

- European debt could sink the global financial system.

And the list goes on... This is certainly NOT a long-term bull market, and the benefits of a buy-and-hold strategy are slim to none!

Trading Is the Answer

So what is an investor to do with this market full of risk?

In order to be truly successful in today's market, investors need to adapt a more nimble approach. They need to become traders!

I'm not saying you need to fire up a high-powered computer and begin entering orders each and every day. You probably don't have time for that. As a professional investor even I don't have time for all that action...

Trading is much less about the amount of activity, and much more about the profit opportunity. To survive in our turbulent economic environment, you need to be able to capture the opportunity that markets present -- and sit on the sidelines when the opportunities aren't good.

For me, this means watching the price action and taking a few key positions each week. And it means trading in sync with the market, whether prices are rising or falling. I'm just as comfortable making money off a falling retail stock as I am buying a precious metal miner. I'm also just as comfortable holding a position for a few days as I am holding for a few months.

It all depends on the opportunity!

Take Sears Holdings (SHLD:NASDAQ) for instance. On June 22, I recommended readers of my Velocity Trader service take a short (bearish) position on Sears. The retail company has been under pressure and was primed for another wave of selling.

To our delight, the very next day Sears dropped sharply and our bearish bet was up 44%. As a trader, when I have an overnight gain of 44%, I like to take some of the profits off the table. It just makes sense to ring the register when the market gives you that much of an advantage.

But at the same time, I still believe Sears has much farther to fall. The company's challenges are still in play, and investors are still likely to sell their shares and push the stock lower. So we only sold half of our position and let the rest run for much larger profits.

Volatility Means Opportunity

That's how the trading game is played. You isolate opportunities, and then you execute. When you have profits, you capture them. You manage your losses and continually monitor the markets for new setups.

Being a trader gives me a distinct edge over "buy and hold" investors. You see, volatility is my friend. When stocks begin to make wild moves, that's when I am able to step in and make a buy or sell transaction and see my profits begin to accumulate.

Buy-and-hold investors simply have to ride out the roller coaster. And watching your net worth bob up and down like a yo-yo is no fun at all... Just ask George.

You see, it does very little good to monitor every tick and tack of a company that you like -- unless you are going to act on the information. As a trader, I continually monitor a watch list of about 85 to 100 stocks, and rotate which stocks are on my list based on what type of opportunities the market is giving.

Your Stocks, Your Decision

Would you indulge me in a quick exercise?

Write down the ticker symbol of the three largest positions in your account. (If you're not holding any stocks, write down three trades you are interested in.) Now next to the ticker, briefly summarize why you like this stock and what you expect the stock to do.

Now keep that sheet next to your computer or in your top desk drawer. Look at it each day. Ask yourself if your reasoning for holding this stock is still valid. Ask yourself if it is still the best opportunity for your money. Ask yourself if it has already accomplished what you expect it to.

If you find that your stock has already served its purpose, or that your original investment thesis is no longer valid, then it's time to move on. Sell that position and look for the next opportunity.

And voilà! You're a now trader!

Editor's Note: Zach is right. Buy-and-hold investing is dead. But it is not bad news, at least for Zach and his Velocity Trader subscribers. As a former hedge fund manager, Zach knows the tricks and techniques it takes to get ahead of the market.

He just released his latest report to his readers. The green light is flashing on a set of potentially huge trades. To read the details, follow the link.

Article brought to you by Taipan Publishing Group. Additional valuable content can be syndicated via our News RSS feed. Republish without charge. Required: Author attribution, links back to original content or www.taipanpublishinggroup.com.

via countingpips.com

Interesting and perfectly valid view point. We are going to cover these view points in great depth in our upcoming courses. There has been a trend in recent years to move towards more frequent buying and selling rather than the traditional buy and hold strategy. We would agree that in today's volatile stock markets, to be a successful trader, you need to adapt a more proactive and disciplined approach. We will cover some key tips on staying disciplined in our upcoming lesson.

The 360 Investing Guys hold no positions in any of the stocks mentioned in this article nor is this article a recommendation to buy or sell.

Wednesday, July 6, 2011

Penny stocks' trades don't make sense

I've got a friend who's intrigued by penny stocks. He's invested in a number of tiny companies whose shares sell for next-to-nothing. As for returns, he's had some big winners and some losers. What's your take on penny stocks? Are they risky?

Penny stocks are stocks of public companies that trade for less than $1 per share. Typically when you purchase a penny stock, you are gambling, not investing.

To answer your question: Yes, penny stocks are risky, for a number of reasons.

Penny stocks trade on a market exchange that is mostly unregulated by the Securities and Exchange Commission. The chances of finding a legitimate penny stock are very low.

Most penny stocks are shell companies whose value goes up and down rapidly because of the individuals trading them. They can be up 200 percent one day and down 80 percent the next, though nothing occurred in the company.

Typically, penny stocks have very low daily volume. This means you could buy and own shares, but, in some cases, have no one to sell them to. You need good liquidity in a stock, especially where the stock price can tank quickly.

Penny stocks differ from most stocks in that they have little or no following by analysts. You will rarely see a stock analyst, wire house or investment bank initiate coverage on a penny stock. Unfortunately, most of the penny stock information on blogs and websites is from individuals whose opinions are based on manipulation or touting a particular stock, vs. factual analysis.

One of my greatest concerns about penny stocks is that their price is easily manipulated. Since they have such a low share price and/or very few outstanding shares, people can easily manipulate the price by placing large buy or sell orders.

A common tactic by scam artists is called a "pump and dump." They buy many shares of a penny stock at a low price and then pump up the price by sending emails and advertisements to unsuspecting investors about this "hot stock." The victims buy into the hype, purchasing the shares and driving up the price significantly. The scam artists then sell their shares for a large profit, leaving the victims with large losses as the stock price heads south.

With penny stocks, you risk failure most of the time. Once in a while, you might get a large return if the company goes big. But over time, the losers outnumber the winners. You're much better off investing in regulated companies with a proven track record.

My advice is to stay far away, unless you are completely fine with losing most of your money.

Jeffrey DeBoer © Copyright The Sacramento Bee. All rights reserved. Original article: http://www.sacbee.com/2011/07/06/3750002/penny-stocks-trades-dont-make.htmlFor those beginners who are looking to invest in penny stocks, an interesting read from Jeffrey DeBoer. Penny stocks are highly speculative and absolutely not recommended for beginner investors. It's easy to get sucked in to the hype when it comes to penny stocks but you take significant financial risk when you buy these stocks. Often penny stocks trade on over the counter (OTC) exchanges as well. These exchanges have less regulatory hurdles than larger exchanges which often creates opportunities for management to 'get away' with alot more than they otherwise would. We will cover OTC exchanges in our upcoming webinars and look forward to discussing the downside to penny stocks with you more!

Sunday, July 3, 2011

How to Make Big Bucks with little risks using Value Investing

How to Make Big Bucks with little risks using Value Investing

Article by Alan McKnight

For those who want to invest with little risk but eventual large returns, the practice of looking for temporarily low priced stocks from valued companies is a great place to begin. The practice, known as value investing is one that has been practiced for years and can result in great success with only a little background in the practice.

If you want to earn money from the stock market and be well on your way towards a nice retirement without taking large risks you may want to look into value investing. When used properly, the value investing stock strategy allows you to safely trade using a basic proven formula that offers little risks but large returns over time.

At the core of the value investing strategy is looking for stocks that are being traded well below what they are worth inherently. In other words, you simply need to find well established companies that have temporarily dipped on the stock market that have historical strengths. This is due to the fact that when the company bounces back, as history demands it will, you will have valuable stocks in your hands that you can trade out for a profit.

In order to find such stocks however, you need to look for strong fundamentals, not just low stocks. This is because cheap stocks are not always great bets, in fact, most of the time buying cheap stocks exclusively can be a large risk that might not always pan out because not every startup company will perform like Apple.

Instead, you want to buy cheap stocks of companies that offer strong historical performance in terms of dividends, earnings, cash flow, and book value. The trick is finding one for a company that is struggling making the stock buy ins cheap at the moment.

A great example of this is McDonalds, which historically was a strong stock that dipped in the nineties but currently is holding tight at the top of the stock market. Everyone who used value investing techniques during the nineties period when stock values dipped is now sitting happily on either a cashed out investment or a solid position in the stock market.

A true stock trader using the value investing strategy will be looking for companies that have undervalued stock shares on the market currently but great potential making them potential gold mines in the future as the share price starts to grow. Of course, you will need to stay up in the business news in order to know what a safe dip is and what a risky dip may be, because if the shares are dropping because of a fundamental problem or scandal the company may not be a wise choice even if it looks great on paper.